VAT in Belgium 2026

VAT in Belgium is TVA, a value-added tax based on a standard rate of 21% and reduced rates of 12% and 6%. This guide explains Belgian VAT rates and rules for businesses, including OSS, warehousing, reverse charge, import VAT, and the ET14000 permit.

We have prepared it for companies selling B2C/B2B to Belgium, using VAT OSS, local warehousing, importing or declaring VAT abroad.

VAT rates in Belgium 2026 – full overview

In 2026, a standard rate of 21% and reduced rates of 12% and 6% will apply in Belgium . The basis for classification is Belgian Royal Decree No. 20 on VAT rates , and when selling cross-border, it's also worth checking the current rules for a given category of goods or services. A 0% rate may apply to certain exceptional goods and services . This should not be confused with the export or IDT exemption.

Applies to goods and services that are not covered by a reduced rate or specific exemption. In 2026, it will include, among others, selected categories related to fossil fuels.

Applies to selected services and goods, e.g. some catering or construction services, if the conditions specified in Belgian regulations are met.

It may include, among other things, selected food products, books, medicines, heat pumps and some works relating to real estate, in accordance with the annexes to the regulations.

What to watch out for when classifying?

The Belgian changes announced apply to, among other things, hotels, campsites, recreational facilities, sports and cultural services, takeaway meals, soft drinks, and pesticides. The Monitoring Comité/BOSA. Before implementing rates in a store or marketplace, it's worth confirming the classification, as the final application depends on the specifics of the product and service.

| Rate type | Height | Most common use | Practical note |

|---|---|---|---|

| Standard | 21% | Most goods and services in Belgium. | Use it if a category is not explicitly covered by a reduced rate. |

| Reduced | 12% | Selected services and goods, e.g. some restaurant, catering and construction services. | Requires verification of conditions from implementing regulations. |

| Reduced | 6% | Selected basic necessities, books, medicines, some works and goods from preferential lists. | The greatest risk of error is with borderline products and sets. |

When might a foreign company need a BE VAT number?

A foreign company should register for VAT in Belgium if it carries out transactions there for which it is obliged to settle Belgian VAT itself, and this obligation is not eliminated by reverse charge, OSS, SME or other appropriate simplification, including the simplification for triangular transactions.

The Belgian VAT number has the format BE + 10 digits, for example BE0123456789.

Storing goods in a Belgian warehouse, also under an FBA or 3PL model, may create local VAT obligations.

The transfer of stocks from another EU country to Belgium may require the transaction to be recorded on the Belgian side.

Intra-Community acquisitions of goods in Belgium may result in the obligation to identify and settle VAT locally.

The introduction of goods into the EU via Belgium requires an analysis of the import VAT and the subsequent sales model.

The sale of goods already located in Belgium may require settlement of Belgian VAT.

A BE VAT number may be needed if the obligation is not eliminated by OSS, cross-border SME, reverse charge or other appropriate simplification.

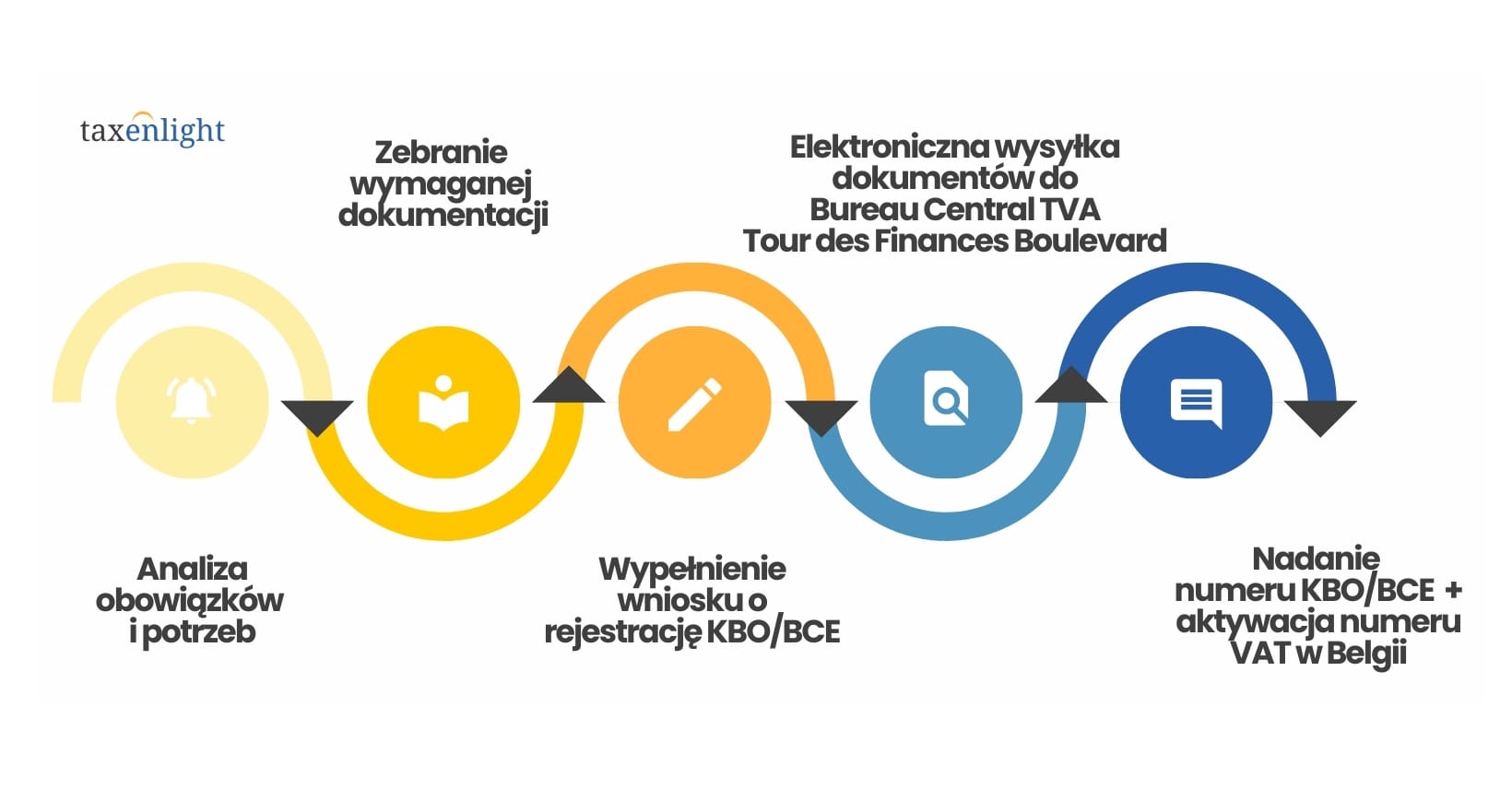

The detailed procedure, required documents and steps for obtaining identification are described in the article VAT registration in Belgium.

Your business may need Belgian VAT identification?

Please see the separate guide on the obligation and procedure for obtaining a BE VAT number.

How does a foreign company settle Belgian VAT?

A company with a BE VAT number may be required to periodically declare and pay Belgian tax, and submit supplementary reports. The scope depends on the type and frequency of transactions.

The proper settlement rhythm depends on the conditions provided for a given taxpayer.

The tax due for a given period must be paid in accordance with Belgian rules.

Report for intra-Community B2B supplies of goods and services, similar to the Polish VAT-EU information.

The list may include Belgian VAT customers who meet the reporting conditions.

Once the relevant thresholds are exceeded, an obligation to submit monthly statistical reports may arise.

Detailed deadlines, reports and shipping methods are described in the article VAT declarations in Belgium.

VAT settlement risks and INTRASTAT obligation

Delays, missing reports, or inconsistent data can result in interest and penalties. Therefore, companies should determine their Belgian obligations before starting sales, imports, or storage.

Reporting when thresholds are exceeded

A company trading goods with other EU countries may be required to submit monthly INTRASTAT reporting after exceeding the relevant thresholds.

Sales, warehouse and customs data should correspond to the values reported in VAT settlements.

The obligation is assessed separately for the relevant directions of goods flow.

The exact thresholds, deadlines and corrections are described in the article settlement by Intervat.

E-invoicing and VAT refund in Belgium

Belgian B2B e-invoicing rules are changing from 2026. At the same time, it's worth streamlining VAT deductions and refunds, as the Belgian administration requires accurate invoices and a link between purchases and business activity.

E-invoices from January 1, 2026.

Belgium has been applying the structured e-invoicing requirement for covered domestic B2B transactions since 1 January 2026. A foreign taxpayer with a BE VAT number who has neither a registered office nor a fixed establishment in Belgium is currently exempt from this requirement solely because of their Belgian VAT registration.

Return in the declaration

A company with an active BE VAT number can carry forward VAT to the next period or apply for a refund as part of the declaration if it meets the deduction conditions.

Return without Belgian number

An EU entity without an active VAT number in Belgium can use the VAT-REF procedure. The standard deadline for submitting a request is September 30 of the year following the year of purchase.

Conditions for deducting VAT in Belgium

- The invoice must be issued to the company's name and relate to purchases related to taxable activities.

- The document should contain the required formal data, including the contractor's correct VAT number, if required.

- The purchase cannot fall into a category with a limitation or exclusion of the right to deduction.

- In the case of external procedures, the office may request additional explanations or copies of documents.

Mail order and warehousing of goods in Belgium

For B2C sales to Belgium, VAT OSS can be used , but only in the appropriate model. Warehousing goods in Belgium, FBA/3PL, or local sales from a Belgian warehouse may require a BE VAT number .

B2C Sales to Belgium

Once you exceed the EU threshold of EUR 10,000, you can settle Belgian VAT via OSS if you do not have local transactions requiring a BE VAT number.

FBA, 3PL, call-off stock

Physical storage of goods in Belgium will usually trigger local VAT obligations, regardless of the distance selling limit.

Warehouse transfers

The transfer of goods between EU countries may involve non-transactional ICS and ICS, which must be included in declarations.

How to recognize that OSS is not enough?

If the goods are located in Belgium before sale, are imported there, or marketplace reports indicate a Belgian warehouse, OSS alone may not be sufficient. In such cases, it is necessary to determine whether local VAT liability arises.

Reverse charge in Belgium and deferred VAT import – ET14000 permit

The Belgian system provides for a reverse charge mechanism for selected B2B transactions and the settlement of import VAT in the declaration after obtaining an ET14000 permit. These are two different institutions, but both are important for foreign companies operating in Belgium.

When can the reverse charge be applied?

Reverse charge can transfer the obligation to settle VAT to the Belgian buyer when the supplier is not established in Belgium and the conditions for the specific transaction and the status of the recipient are met. The mechanism does not automatically apply to all B2B sales.

When is reverse charge not enough?

If the transaction is local, concerns a sale from a Belgian warehouse, import, event or service taxed locally without passing on the obligation to the purchaser, a BE VAT number may be needed.

What is deferred VAT import?

The ET14000 permit allows you to settle import VAT in your Belgian periodic declaration instead of paying it at customs. This mechanism is not applied automatically – you must obtain the permit before you begin settling it.

Conditions for the use of the ET14000 permit

- Active VAT BEThe company must be an active VAT payer in Belgium.

- EORIYou need an EORI number linked to your Belgian VAT number.

- Permissionmust be obtained before using the import VAT settlement in the declaration.

- Periodic declarationsThe company must submit Belgian periodic declarations and report VAT imports therein.

Do you have sales, warehouse or import in Belgium?

We will check the appropriate VAT rates and rules, the application of OSS or reverse charge, and the effects of warehousing and import, including the possibility of obtaining an ET14000 permit.

VAT in Belgium 2026 – what to remember?

The standard VAT rate in Belgium is 21%, with reduced rates of 12% and 6%.

Warehousing, import, intra-Community acquisition and local sales may result in the obligation to register for Belgian VAT.

The scope of responsibilities depends on the transaction model and the BE VAT number.

OSS can help with B2C, but does not replace local VAT for warehousing or local transactions.

The ET14000 permit may enable the settlement of import VAT in the Belgian periodic declaration after meeting the required conditions.

The most important thing is to correctly determine the place of taxation and maintain consistent data.

VAT in Belgium 2026 FAQ – Frequently Asked Questions

In Belgium, a standard rate of 21% and reduced rates of 12% and 6% apply. For certain exceptional goods and services, a 0% rate may apply, which should not be equated with an export or IDT exemption.

A foreign company should register for VAT in Belgium if it carries out transactions there for which it is obliged to settle Belgian VAT itself, and this obligation is not eliminated by reverse charge, OSS, SME or other appropriate simplification.

A foreign company not established in Belgium does not automatically benefit from the Belgian exemption. However, a company established in another EU country can apply for the cross-border SME exemption if it meets the EU-wide turnover limit of €100,000, the Belgian limit of €25,000, and other conditions and receives EX identification.

Yes, storing goods in Belgium, using FBA or 3PL and selling from a Belgian warehouse may trigger local VAT obligations which OSS does not replace.

Not always. VAT OSS can be used to settle B2C sales to Belgium, but it does not replace local registration for a Belgian warehouse, local sales, imports, or other activities requiring a BE VAT number.

Belgium has been applying the structured e-invoicing requirement for covered domestic B2B transactions since 1 January 2026. A foreign taxpayer with a BE VAT number who has neither a registered office nor a fixed establishment in Belgium is currently exempt from this requirement solely because of their Belgian VAT registration.

The method of recovering the tax depends on whether the company settles Belgian VAT locally. An EU entity without a Belgian VAT registration can, under certain conditions, use the VAT-REF procedure.

Reverse charge can transfer the obligation to settle VAT to the Belgian buyer when the supplier is not established in Belgium and the conditions for the specific transaction and the status of the recipient are met. The mechanism does not automatically apply to all B2B sales.

The ET14000 permit allows you to settle import VAT in your Belgian periodic declaration instead of paying it at customs. It requires the submission of Belgian periodic declarations, an EORI number linked to your Belgian VAT number, and authorization before you can use this settlement.

Importing goods into Belgium generally triggers import VAT. After obtaining an ET14000 permit and meeting its requirements, a company can settle the tax on its Belgian periodic declaration instead of paying it at customs.