VAT rates in the European Union 2026

EU VAT rates in 2026 vary by country, product or service category, and transaction type. This table helps you quickly check the standard and reduced VAT rates in European Union countries.

The list is particularly useful for companies settling VAT OSS declarations, cross-border sales and VAT declarations abroad.

EU VAT rates 2026: current table

The table includes standard, reduced, and super-reduced VAT rates in European Union countries. The data is particularly useful for B2C sales, OSS billing, and rate configuration in marketplaces and accounting systems.

| Country | Country code | Standard | 1. reduced | 2. reduced | Super reduced |

|---|---|---|---|---|---|

| Austria | AT | 20% | 13% | 10% | — |

| Belgium | BE | 21% | 12% | 6% | — |

| Bulgaria | BG | 20% | 9% | — | — |

| Croatia | HR | 25% | 13% | 5% | — |

| Cyprus | CY | 19% | 9% | 5% | — |

| The czech republic | CZ | 21% | 12% | — | — |

| Denmark | DK | 25% | — | — | — |

| Estonia | EE | 24% | 13% | 9% | — |

| Finland | FI | 25,5% | 13,5% | 10% | — |

| France | FR | 20% | 10% | 5,5% | 2,1% |

| Greece | EL | 24% | 13% | 6% | — |

| Spain | ES | 21% | 10% | 4% | — |

| Netherlands | NL | 21% | 9% | — | — |

| Ireland | IE | 23% | 13,5% | 9% | 4,8% |

| Luxembourg | LU | 17% | 14% | 8% | 3% |

| Lithuania | LT | 21% | 12% | 5% | — |

| Latvia | LV | 21% | 12% | 5% | — |

| Malta | MT | 18% | 7% | 5% | — |

| Germany | DE | 19% | 7% | — | — |

| Poland | PL | 23% | 8% | 5% | — |

| Portugal | PT | 23% | 13% | 6% | — |

| Romania | RO | 21% | 11% | — | — |

| Slovakia | SK | 23% | 19% | 5% | — |

| Slovenia | AI | 22% | 9,5% | 5% | — |

| Sweden | SE | 25% | 12% | 6% | — |

| Hungary | HU | 27% | 18% | 5% | — |

| Italy | IT | 22% | 10% | 5% | 4% |

Note: The table shows the main rates. The scope of application of reduced rates depends on local regulations and the product or service category.

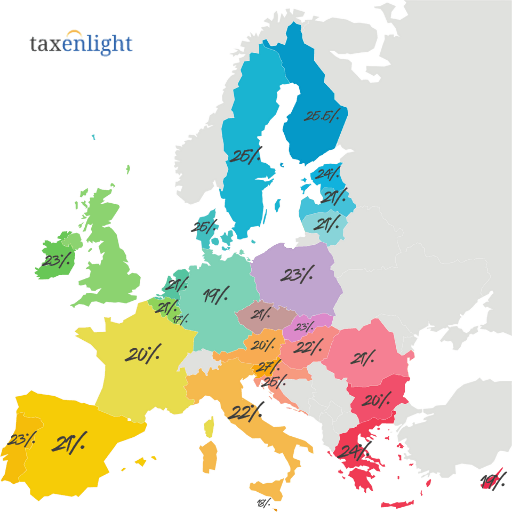

2026 EU VAT rates - interactive map

Check the standard VAT rates for European Union countries on a map. This is a quick way to compare tax burdens between countries and determine which rate to apply when selling cross-border.

EU VAT rate changes: what's changed in 2025?

Some of the changes introduced in 2025 will also apply in 2026. For businesses, this means updating rates in sales systems, marketplaces, cash registers, and OSS billing tools.

Slovakia

The standard VAT rate is 23%. Reduced rates of 19% and 5%.

Estonia

The standard VAT rate is 24%. The table also includes reduced rates of 13% and 9%.

Romania

The standard VAT rate is 21%and the main reduced rate is 11%.

VAT rates in the EU and VAT OSS

Under the VAT OSS , the seller settles B2C sales to other EU countries in a single declaration, but applies the VAT rate of the country of consumption. This means that when selling to multiple countries, the rates for each country must be correctly assigned.

As a rule, the rate of the country of establishment can be applied if B2C sales to other EU countries do not exceed the combined threshold.

You must use the VAT rates of the recipient countries and settle sales through OSS or local VAT registrations.

If you store goods in another EU country, the OSS procedure alone will not usually replace local VAT registration abroad.

VAT OSS and VAT rates – example

A Polish company sells products to consumers in Germany and France. Above the €10,000 threshold, it should apply the appropriate rates in the recipient country: for example, 19% German or 20% French, unless the product category in question benefits from a reduced rate.

How are VAT rates determined in the European Union?

The European Union establishes the framework for the VAT system, but the specific rates are set by the Member States. Therefore, there is no single common VAT rate within the EU, and the rate tables must be regularly updated.

The basic principles stem from Directive 2006/112/EC. It establishes a framework for standard rates, reduced rates, and exceptions.

Each EU country determines the list of goods and services covered by reduced rates, within the limits of EU law.

When selling in the EU, it is worth using official sources, such as the Your Europe website about VAT rules.

Do you sell to several EU countries?

We help you determine the correct VAT rates, select an OSS or local VAT registration, and organize your settlements in EU countries. This is especially important if you sell through a marketplace, store goods abroad, or have multiple product categories.

VAT rates in the EU 2026 – the most important conclusions

Each country has its own rates, so when selling internationally, knowing one country's rate is not enough.

Once the B2C sales threshold of EUR 10,000 is exceeded, the VAT rates of the recipient country must be applied and correctly reported in the OSS.

Just because a country has a reduced rate does not automatically mean that it covers a given product or service.

Rates need to be updated across stores, marketplaces, invoicing, and accounting systems to avoid adjustments and backlogs.

VAT rates in the EU 2026 - FAQ

Yes. The OSS VAT return applies the rates of the country of consumption, i.e., the recipient country. The table helps you check the basic rates, but for a specific product, you need to confirm whether a reduced rate applies.

Yes. Member States can change VAT rates throughout the year. Therefore, companies selling to multiple countries should regularly update their sales and accounting systems.

It's safest to use official sources from the European Commission, local tax administrations, and current expert studies. For unusual goods, it's worth checking local classifications.

This is an exceptionally low VAT rate applied only in selected countries and for limited categories of goods or services. Not every EU country has this rate.

Most often, after exceeding the total threshold of EUR 10,000 of B2C sales to other EU countries or after voluntarily choosing to settle sales according to the rules of the country of consumption.

Yes. Registering for VAT OSS can be voluntary. This is convenient for some companies, as it allows them to apply the recipient country's rates from the outset and avoid changing their settlement model mid-year.

Incorrect rates can lead to declaration corrections, additional tax payments, interest, penalties, and problems with the OSS process. The risk increases with a large number of transactions and marketplace sales.

Yes. Digital and electronic services provided to consumers in the EU are generally taxed in the country of consumption and may be accounted for through VAT OSS.